In the race to lock up marquee backers and broadcast unicorn status, AI startups are quietly adopting a split-pricing playbook: issuing the same series of preferred shares in the same round at two different prices. The tactic creates a splashy “headline” valuation for latecomers while giving the lead investor a discounted entry—manufacturing the optics of market leadership without requiring two separate financings.

How Split Pricing Works Inside One Round

Mechanically, companies run multi-close rounds. The lead investor anchors a first close at a lower price per share, often paired with rights like pro rata expansion or warrants that further reduce their effective cost. Subsequent closes, sometimes only weeks later, are sold to additional funds at a higher price but under the same series label. Everyone receives the same class of preferred; the difference is what they paid to get it.

Variations abound. Some deals use a “first-close discount” or step-up grid (for example, the first $50 million at one price, the next $25 million at a premium). Others staple small warrant coverage to the lead, creating a shadow discount. In hot processes, founders even admit oversubscribed investors immediately—at the premium price—rather than pushing them to a future round.

Why Founders Offer Discounts To Lead Investors

In today’s AI land grab, a top-tier lead confers more than cash. Their brand helps recruit scarce researchers, win enterprise pilots, and tee up future capital. That signaling power is why founders accept a lower effective price for the lead and charge everyone else more. It also lets them print a bigger valuation number without the time sink of running back-to-back rounds.

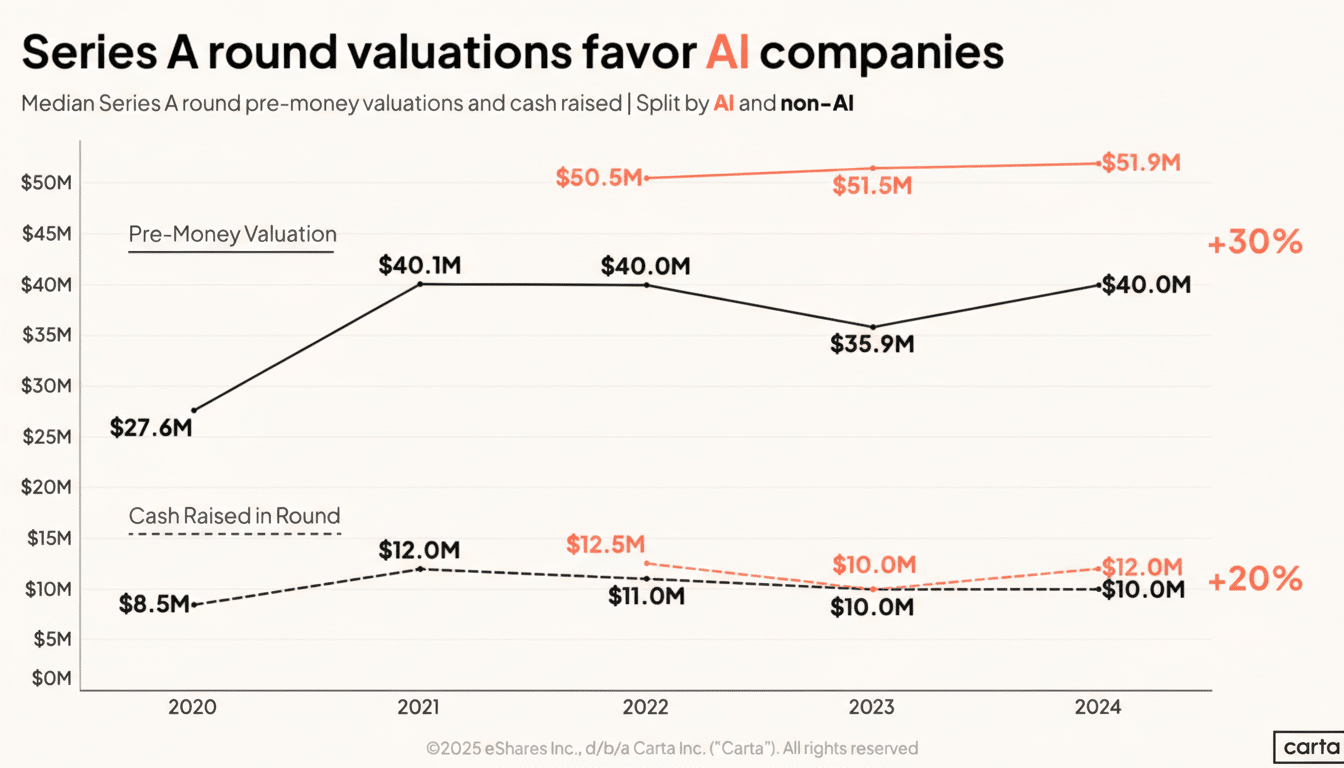

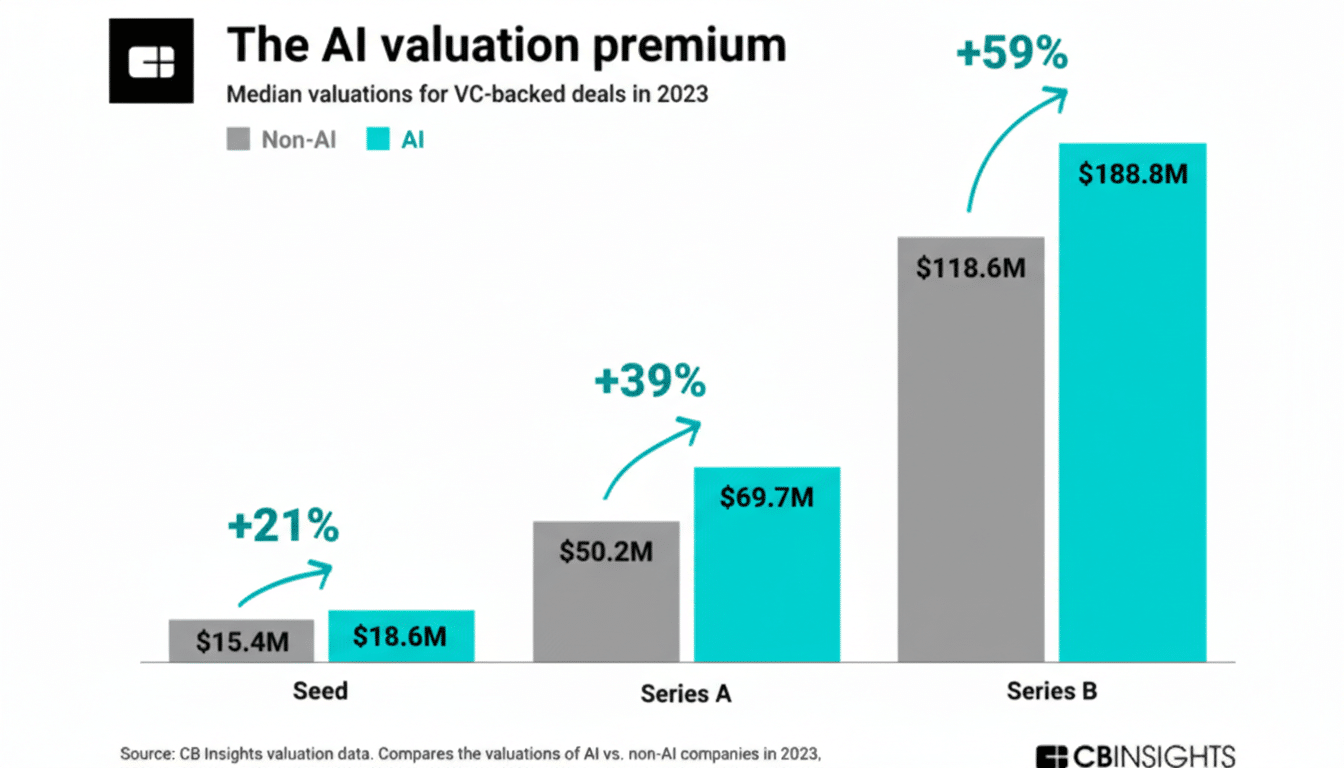

Carta’s fundraising reports have shown that AI companies, on average, command larger step-ups than general software peers, and competitive dynamics are a major reason. PitchBook has also flagged a rise in structured features—like warrants and multi-close rounds—used to win allocation in sought‑after AI deals. The end result is the same: the blended price on the cap table is meaningfully below the headline valuation touted in press releases.

The Optics And The FOMO Engine Driving AI Rounds

Perception matters in winner-take-most AI categories. A unicorn label deters rivals’ fundraising, sways procurement teams, and rallies recruits. Investors know it. A lead that buys early at a discount still benefits from the aura of a billion‑dollar round when it publishes the mark to its LPs.

Recent examples illustrate the playbook. Serval, an AI IT help desk startup highlighted by the Wall Street Journal, let its lead invest at a valuation reported around $400 million while announcing a $1 billion Series B after bringing in additional investors at the higher price. Another buzzy startup, Aaru, reached unicorn headlines even as a large tranche of its round cleared below that level. The strategy trades pricing purity for speed, scarcity, and splash.

Venture veterans are split on the practice. Some, like partners at Primary Ventures, argue that aggressive headline marks can freeze out capital for runners‑up by signaling a dominant winner. Others, including managers at FPV Ventures, warn that selling the same shares at two prices feels like bubble behavior, even if it’s technically clean and board‑approved.

What Buyers Are Really Paying For In These Rounds

Investors accepting the higher price aren’t just buying equity; they’re buying access. In a cap table with limited seats, paying a premium secures an early line of sight into customer traction, a relationship with the founding team, and a chance to lead the next round. For multistage firms, the option value of staying close to a potential category leader can justify a 10%–30% step‑up within the same series.

For leads, the discount is compensation for underwriting risk, doing the diligence, and helping close the syndicate. For founders, consolidating demand now lowers execution risk later—no six‑month gap between rounds, no window for competitors to catch up.

Hidden Risks And Governance Considerations

The math eventually has to reconcile. If a company’s next raise does not clear the inflated headline price, it courts a down round—painful dilution for employees and a hit to credibility with customers and partners. Operators who navigated the 2022 reset, including managers at Thiel Capital, caution that chasing extreme marks turns a growth plan into a high‑wire act.

There are also cap table and legal wrinkles. Differential pricing can trigger MFN clauses in earlier SAFEs if not structured carefully. Extra warrants or preferences for the lead can shift effective economics, complicating future pro rata math. While Delaware law allows boards to issue the same class at different consideration, directors still owe duties of fairness to all stockholders. Transparency in board minutes and robust process records matter.

Internally, headline valuations can lift 409A appraisals, nudging option strike prices higher and dulling the equity carrot for new hires. Finance teams should emphasize the blended price and use independent valuations to avoid anchoring compensation on PR marks.

What To Watch Next In AI Fundraising Dynamics

Expect more multi-close AI rounds with step-ups as long as oversubscription persists.

Signals to monitor:

- Rising use of warrant coverage in term sheets

- Bigger gaps between first‑close and final‑close prices

- Tighter MFN language in SAFEs

If revenue ramps and model unit economics fail to keep pace, watch for quiet “extensions” that bridge to the next milestone rather than testing those headline marks.

The dual‑pricing era may prove a savvy way to compress time and amplify momentum—or a telltale of froth. Either way, founders and investors are betting that in AI, the perception of being the winner helps make it true. The hard part is making sure the numbers eventually agree.