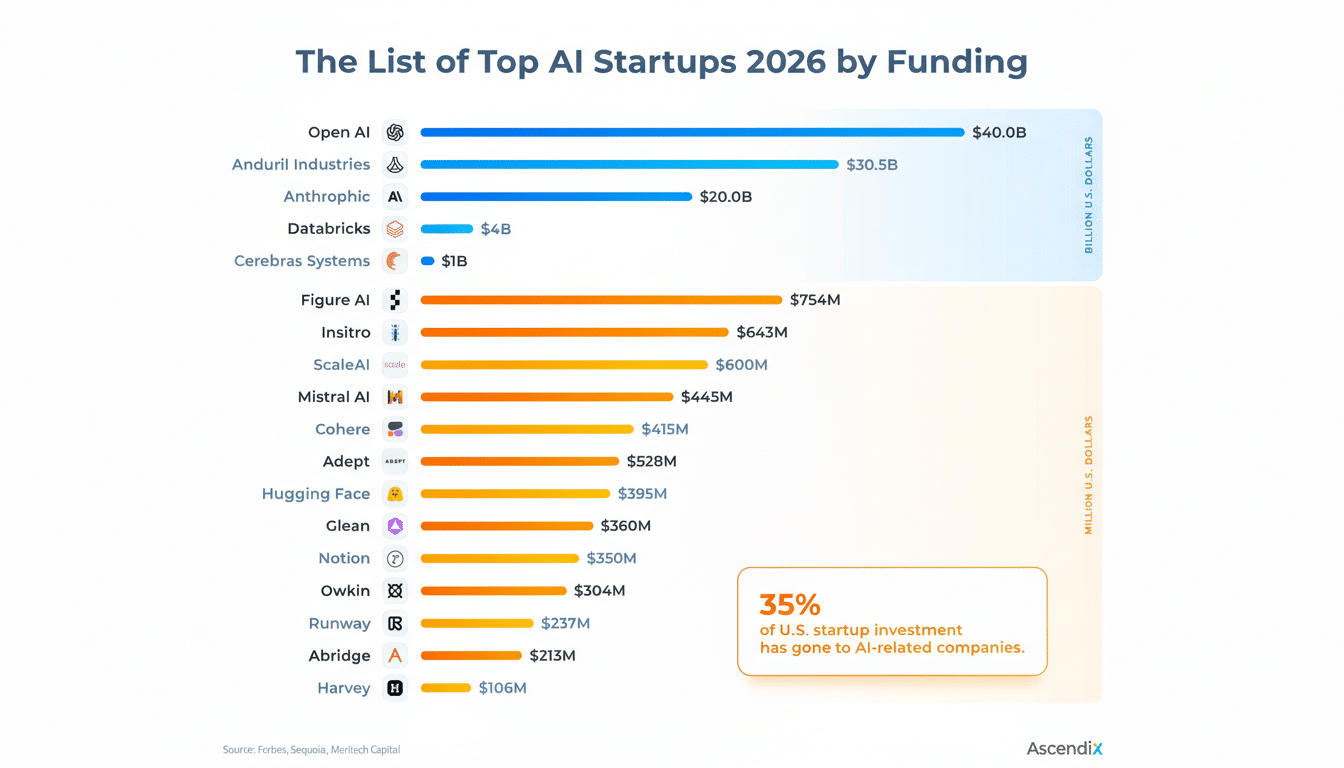

Seventeen U.S.-based AI startups have already secured nine-figure financings this year, underscoring how investor demand for core models, data infrastructure, and applied AI remains resilient even as broader venture activity normalizes. The cohort spans everything from foundation model labs and agent platforms to robotics, healthcare, and fintech applications—each chasing scale, data advantages, and the compute needed to turn prototypes into durable businesses.

Seventeen US AI Mega Rounds at a Glance for 2026

Based on public company announcements and market trackers commonly used in venture capital—such as PitchBook, CB Insights, Crunchbase, and firm-authored press releases—the 17 deals share familiar hallmarks: large equity checks, strategic cloud commitments, and cap tables blending top-tier venture firms with crossover and corporate investors. While the names and round mechanics vary, the strategic intent is similar: lock in compute, compress product roadmaps, and win distribution.

- Seventeen US AI Mega Rounds at a Glance for 2026

- How We Counted US AI Startup Mega Rounds

- Where the Capital Is Flowing Across US AI Sectors

- Who Is Writing the Checks for These Mega Rounds

- Key Signals Emerging From Recent AI Term Sheets

- Why These Nine-Figure AI Financings Matter Now

- What to Watch Next for US AI Funding and Deals

Notably, a material share of these rounds landed in San Francisco and the broader Bay Area, with New York and Boston contributing meaningful activity in enterprise AI, biotech-AI, and fintech-AI. That geographic split tracks with historical patterns: the U.S. has consistently led global private AI investment by value, according to annual analyses from Stanford HAI and industry databases.

How We Counted US AI Startup Mega Rounds

This tally includes U.S.-headquartered companies announcing equity financings of $100 million or more this year, inclusive of priced rounds and primary capital raised via SAFEs or convertibles where the company or investors disclosed size. It excludes pure debt facilities and undisclosed raises. The lens here is startups first—corporate R&D and internal venture efforts are not counted unless capitalized as independent entities.

Round stage labels can be slippery in today’s market, so comparisons focus on substance: new capital closed, investor mix, and strategic commitments like cloud credits or multi-year compute reservations that often accompany mega rounds. Those elements matter more than whether a company brands a financing as Series B, C, or “growth.”

Where the Capital Is Flowing Across US AI Sectors

Foundation and multimodal model builders remain prime recipients. Their burn is compute-heavy, and the race to higher context windows, longer reasoning chains, and tighter tool-use integration continues to reward well-capitalized players. Many of the 17 are using funds to secure GPUs, scale inference clusters, and finance model distillation that cuts latency and cost per token for enterprise workloads.

Agentic platforms and vertical copilots also feature prominently. Startups focused on workflow automation in sales, customer support, software development, and finance are pairing product-led growth with enterprise security and governance. In these cases, nine-figure rounds are less about brute-force training runs and more about data acquisition, SOC 2/ISO maturation, and go-to-market buildout across regulated sectors.

Robotics and autonomous systems surface among the 17 as well, reflecting a durability investors have been seeking: AI that moves atoms, not just bits. Funding is earmarked for perception stacks, simulation, and factory pilots where AI improves pick rates, quality control, or last-10-feet logistics. Healthcare-AI entrants within the cohort are pursuing clinical validation and payer integration, often in tandem with academic partners to ensure their models generalize safely.

Who Is Writing the Checks for These Mega Rounds

Generalist growth funds and crossover investors—those with a public markets toolkit—are heavily represented, a sign that the IPO optionality story is back on the table for select AI leaders. Corporate investors, especially hyperscalers and semiconductor companies, appear not only on cap tables but in commercial schedules: multi-year cloud spend agreements, preferred access to accelerators, and co-selling arrangements aimed at enterprise buyers.

Seed and early-stage specialists are often re-upping to preserve ownership, but the gravitational pull of nine-figure rounds means syndicates skew concentrated. The presence of strategic capital is double-edged: it can turbocharge distribution and infrastructure access, but startups must guard against channel dependency and negotiating leverage that tightens over time.

Key Signals Emerging From Recent AI Term Sheets

Across the 17, diligence has shifted from “demo sparkle” to verifiable unit economics: inference cost curves, gross margin uplift from model optimization, and empirical retention among pilot-to-paid conversions. Boards are pressing for revenue quality—contracts with clear usage floors, data rights clarity, and pathways to deployment in regulated environments. Where valuation terms stretch, investors are offsetting with performance tranches, enhanced information rights, or structured downside protection.

On the technical side, many rounds bake in budgets for retrieval-augmented generation, synthetic data pipelines, and eval harnesses tied to domain outcomes rather than generic leaderboards. That’s in line with insights from the AI Index and enterprise surveys: buyers increasingly select on reliability, security posture, and integration depth over raw benchmark scores.

Why These Nine-Figure AI Financings Matter Now

Nine-figure financings are not just vanity metrics; they dictate the competitive shape of the market. Capital at this scale can secure scarce compute, attract senior engineering talent, and fund multi-year enterprise sales cycles that younger rivals cannot sustain. It also accelerates standards-setting: the platforms in this 17-strong group will influence API conventions, safety practices, and procurement norms adopted by Global 2000 buyers.

For the broader ecosystem, the signal is clear. While venture funding overall has become more selective, AI remains a priority category where investors continue to underwrite ambitious plans—provided the roadmap connects model capability to measurable business value.

What to Watch Next for US AI Funding and Deals

Expect more hybrid deals blending equity and compute commitments, faster cycles on model refreshes that slash serving costs, and a pickup in M&A as well-capitalized players buy data assets or domain-specific teams. Enterprise demand for private deployments—on VPCs or on-prem—will keep rising, rewarding startups that can deliver performance without sacrificing sovereignty or compliance.

If history is a guide, a subset of the 17 will pursue late-stage extensions to accelerate into new markets or acquisitions. The rest will focus on disciplined revenue ramp, seeking the kind of durable growth profile that public investors reward once markets fully reopen. Either way, the early tally confirms it: U.S. AI’s big-check era is still very much alive.