The new headline number of the recovery is this: at least 80 tech companies reached $1 billion valuations this year, according to an aggregate tally from PitchBook, CB Insights and Crunchbase. Fueling the surge has been AI across the stack, a rebound for capital-intensive “hard tech” and a new wave of enterprise software names that expanded efficiently throughout the downturn.

And though the pace calls to mind boom-time memories, the mix is different. More of these new unicorns are hawking infrastructure or mission-critical software; fewer are purely consumer bets, and a bunch made it to the magical valuation threshold on actual revenue rather than speculative growth alone.

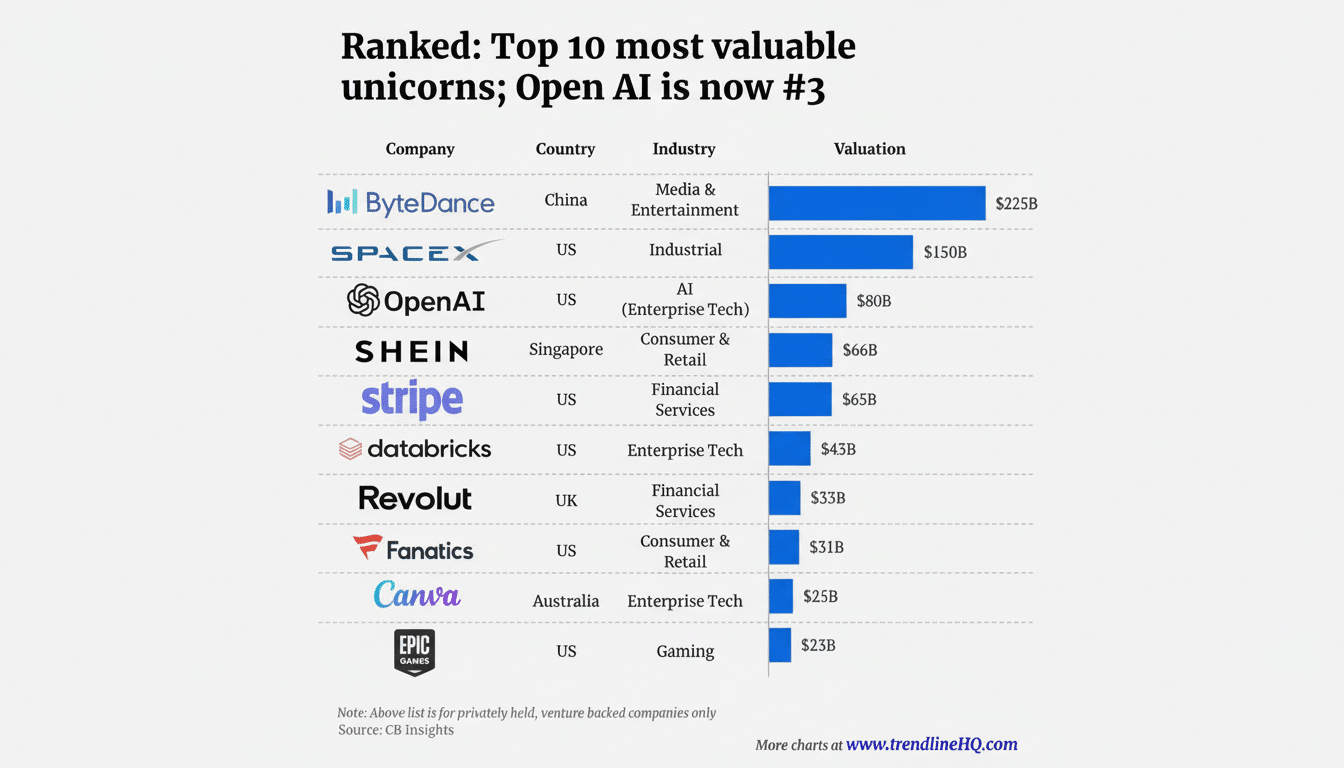

- AI leads the charge as the majority of new unicorns

- Deep tech and space reenter the club as demand rises

- Fintech and crypto reawaken with compliance-first focus

- Healthcare and bio ride AI tailwinds into deployment

- B2B software quietly compounds with efficient growth

- Rounds aside, how do investors mix primary and secondary?

- What comes next for these unicorns and their backers

AI leads the charge as the majority of new unicorns

AI remains the engine. Trackers reveal that well over 50% of newly minted unicorns are AI-native or AI-adjacent, spanning from model labs to inference, data pipelines and agentic workflows. Infrastructure highlights include Fireworks AI, Baseten and Modular that raised large rounds as enterprises make a standard of the serving and monitoring layers over one model bet.

The model builders are still writing big checks: Reflection raised a multibillion-dollar Series B with strategics like Nvidia, and Reka moved while dancing circles around the frontier labs. On the practical side, Decagon and You.com are securing enterprise deals for customer support and workplace AI, while LangChain’s agent engineering tools went from developer curiosity to deployment staples. Investors in these winners include Sequoia, a16z, Benchmark, Lightspeed and Index.

Deep tech and space reenter the club as demand rises

Another clear theme is the comeback of deep tech. Quantum computing player PsiQuantum took a blockbuster round and optical interconnect startup Celestial AI and chip upstart Substrate joined the club amid demand for faster compute and supply chain resilience. Policy tailwinds around semi-sovereignty and industrial capacity have also not hurt.

In space, Stoke’s fully reusable launch plans and Apex’s approach to manufacturing satellites achieved unicorn status as customers moved beyond demonstration missions to constellations and recurring services. Loft Orbital was another hit, as the firm’s turnkey space infrastructure continued to attract demand. This group is capital-intensive, though the visibility of revenue through government and commercial contracts is arguably higher than during the last cycle.

Fintech and crypto reawaken with compliance-first focus

Fintech’s new entrants tend to congregate in infra and market access rather than pure neobanking. Temppo saw its multibillion valuation riding blockchain payments volume, and prediction markets Polymarket and Kalshi were unicornized as traders sought structured access to event risking. A stealthy startup bankrolled with an unusually large seed has emerged out of the shadows.

The theme: compliance-first architectures and business models that monetize throughput & risk management vs. interchange arbitrage. Investors say that underwriting discipline has come back, but payment rails and alternative markets continue to show robust growth.

Healthcare and bio ride AI tailwinds into deployment

The truth is that clinical AI and data-rich drug discovery are venture categories. Ambience and Abridge crossed the chasm based on deployment-ready medical scribe technology, while Hippocratic AI and OpenEvidence moved forward with specialized models focused on workflows that reduce time-to-note and time-to-diagnosis. On the therapeutics side, Enveda, NewLimit and Pathos employed data platforms to speed candidate selection and development.

The buyer here is disciplined. Health systems and payers want cost savings and demonstrable outcomes; for vendors who are winning, it is through the integration with incumbent EHR stacks; tackling privacy up front; or aligning with reimbursement paths. That’s a drastic departure from the early “move fast” experiments.

B2B software quietly compounds with efficient growth

And beneath the splashy AI headlines, a steady parade of workflow platforms pummeled their way into unicorn territory. Filevine in legal, MaintainX and CompanyCam in field operations, and BuildOps in contractor software all combined usage and upsells, then raised growth rounds. It is the case that bottom-up adoption plus usage-based pricing are a winning formula as evidenced by data and product tooling players like PostHog, Hightouch, Statsig and Linear.

In a market that now rewards efficient growth, some of these companies combined strong net revenue retention with improving operating metrics. General Catalyst, Bessemer Venture Partners and GV were among the investors who leaned in across this group.

Rounds aside, how do investors mix primary and secondary?

This year’s unicorn-making rounds were concentrated between $100 million and $500 million, with a handful of outliers at around $1 billion. Market participants, such as Carta and secondary platforms, note more mixed rounds that include both primary capital used to accelerate growth and secondary liquidity for early believers. Structural terms are less common this year, but continue to show up in capital-intensive categories.

Geographically, the U.S. continues to be dominant, but Europe and India also had meaningful shares of LPs and the Middle East is becoming a growth-stage LP hub. Strategic investors — from cloud providers to chipmakers — showed up in AI infra and semiconductor deals, evidence that distribution and ecosystem lock-in is as important as raw tech.

What comes next for these unicorns and their backers

More than 80 fresh unicorns, but can they keep growing? Key watch items:

- Enterprise AI spending beyond pilots

- Quality of gross margin in model-heavy businesses

- Defense and space procurement timelines

- Regulatory clarity for crypto and AI in healthcare

And, as long as IPO and M&A windows continue to thaw, the next class may well graduate faster than the last — so long as growth is met with discipline.