Europe’s university laboratories have turned into a formidable startup engine, with nearly 80 deep tech and life sciences spinouts now clearing either the $1 billion valuation mark or $100 million in annual revenue. Dealroom’s latest European Spinout Report counts 76 companies at these milestones, signaling that academic IP is maturing into scale businesses and a resilient late-stage pipeline investors can’t ignore.

The aggregate value of Europe’s spinout funnel has swelled to an estimated $398 billion, according to the same report, even as broader venture markets cooled. The takeaway is clear: academic commercialization is no longer a side channel—it’s become one of the continent’s most dependable sources of defensible innovation.

- Why spinouts are surging across Europe’s deep tech scene

- New funds target academic IP across Europe’s deep tech

- Standout exits and mega funding rounds across European spinouts

- The growth capital gap holding back late-stage European spinouts

- What to watch next for Europe’s deep tech spinouts and policy shifts

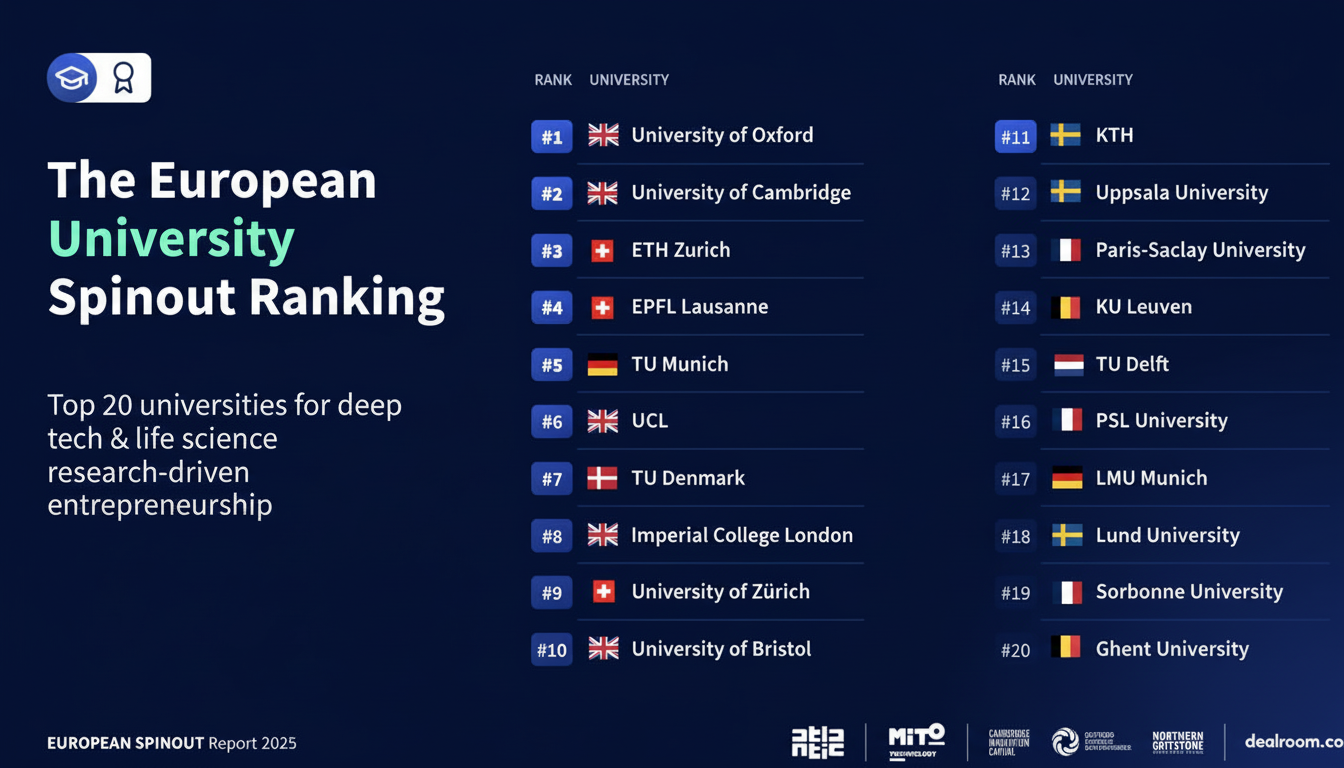

Why spinouts are surging across Europe’s deep tech scene

Deep tech thrives where scientific depth, specialized infrastructure, and patient capital intersect. Europe’s research universities offer all three, and top hubs—led by Cambridge, Oxford, and ETH Zurich—now anchor a long tail of institutions that can take lab breakthroughs to market.

More professional tech transfer, cleaner IP terms, and founder-friendly equity splits have helped. So has the rise of specialist operators who understand timelines for quantum, robotics, semiconductors, advanced materials, climate tech, and biotech. The result is a new class of venture-backable companies built around hard-won scientific advantages rather than purely software distribution.

New funds target academic IP across Europe’s deep tech

New capital is nesting around the spinout opportunity. Denmark’s PSV Hafnium closed an oversubscribed €60 million debut fund to back Nordic deep tech, while University2Ventures (U2V), which has offices in Aachen, Berlin and London, is aiming for a similar fund size following an initial close. Both are positioning themselves to draw from labs that historically haven’t been well connected into venture networks.

They complement established university-affiliated investors like Oxford Sciences Innovation and Cambridge Innovation Capital, and independent funds that now see spinouts as potential fund returners in their own right. The thesis is simple: when product and IP risk have been de-risked with years of research execution, the market comes down to two variables — execution and timing — both of which investors can underwrite.

The model is being compounded beyond the regular suspects. PSV Hafnium itself spun out of the Technical University of Denmark and has already invested in companies like SisuSemi, a Finnish startup using 10 years of research from the University of Turku to make semiconductor surface cleaning better. Expect more regional labs to plug into this pan-European deal flow.

Standout exits and mega funding rounds across European spinouts

The headline names are beginning to resemble household brands in their categories: Iceye in synthetic aperture radar, quantum computing’s IQM, launch venture Isar Aerospace, generative video startup Synthesia and unmanned systems company Tekever have all hit major valuation milestones.

On the other end of the exit spectrum, Oxford Ionics was acquired by IonQ for a multibillion-dollar outcome, one of several spinouts from the U.K., Germany and Switzerland that returned more than $1 billion to investors. And big rounds are falling into capital-intensive arenas — from Proxima Fusion in next-gen energy to Quantum Systems, the dual-use drones startup now valued north of $3 billion.

Even with a broader venture reset, European university spinouts in deep tech and life sciences appear set for near-record fundraising totalling about $9.1 billion, according to Dealroom. The divergence with the market’s slump shows that investors are focusing on core science and dual-use capabilities with long-term defensibility.

The growth capital gap holding back late-stage European spinouts

The weak part of the chain is late-stage capital. Close to half of all growth funding for European deep tech and life sciences spinouts is still attracted from beyond the region, most commonly the U.S., said Dealroom. That reliance has gone down but is still significant, so Europe is still exporting some of the upside generated by its own public research budgets.

Addressing this will require:

- Individual European ecosystems may each need to mature and develop by drawing from deep domestic growth equity pools, matched with scaled commitments by institutional LPs alongside catalytic participation from organizations like the European Investment Bank and the European Innovation Council Fund.

- Deepening domestic growth equity pools

- Scaled commitments from institutional LPs

Public procurement and defense-led demand can also de-risk the scale-up in dual-use sectors, crowding in private growth investors.

What to watch next for Europe’s deep tech spinouts and policy shifts

Policy adjustments such as standardizing university IP terms, opening access for researchers to more equity and streamlining the formation of spinouts could open up the funnel even more. Second-generation founders who’re recycling early expertise with “lab” companies ought to help broaden this map geographically, significantly into the Nordics, DACH, Benelux and Southern Europe.

If positive momentum continues, then the convergence of maturing science and specialist capital along with international customer pipelines means Europe’s spinouts are to convert more of the Continent’s research base into truly globally relevant companies. Hitting $1 billion valuations or having $100 million in revenue is no longer the exception in this sliver of the ecosystem; it’s starting to become the norm.