Hydrocarbons are becoming compute. A new analysis by the International Energy Agency shows that investment in data centers is spent at no less than $580 billion this year, some $40 billion more than was spent on building new oil supplies. The crossover highlights how AI and cloud services have transitioned from optional upgrades to integral infrastructure.

Why compute is the new money magnet for global investors

Demand surges following AI training and inference are creating new capacity planning challenges, shaping demand for data center space. In contrast to oil exploration, for which cash flows can swing with commodity cycles and drilling successes or failures, digital infrastructure tends to involve multi‑year contracts, high utilization and predictable returns. The latter is attracting private equity firms, infrastructure funds and sovereigns directly into a previously niche asset class.

- Why compute is the new money magnet for global investors

- Where the global data center buildout is focused

- Why electric power access is the new permitting hurdle

- The energy mix driving the data center buildout boom

- Why the oil investment comparison matters right now

- What to watch next as compute outspends oil globally

Cloud provider earnings calls are indicating record investment, and specialist facility operators report full build-to-suit pipelines as well. The framing in the IEA is telling: data centers are not a support act — they are now a destination for global infrastructure capital.

Where the global data center buildout is focused

New electricity demand from data centers will occur in the U.S., with most of the rest divided between Europe and China, according to estimated figures from the IEA. Most growth is clustering around major metropolitan areas — the vast majority of new projects are in cities with a population of more than 1 million, where fiber density, talent and proximity to customers help minimize latency and cost.

Scale is accelerating. About half of the backed projects in development are 50-plus megawatts, with many built next door to an existing campus in order to connect nodes or utilities. That clustering bolsters the economics — but it concentrates risk in several grid-constrained regions.

Why electric power access is the new permitting hurdle

And as the sector outspends oil exploration, the crucial bottleneck isn’t rigs — it’s electricity. The IEA points to growing grid congestion and deep interconnection queues in several jurisdictions. In portions of northern Virginia, developers can be mired in waits that extend over a year to a decade. One of Europe’s largest electricity hubs, Dublin, has stopped new grid connections until 2028 to deal with local constraints.

Supply chains add friction. High-voltage cables, transformers, gas turbines and critical minerals for batteries are running late, hampering substation upgrades and backup generation. This is where emerging tech could come in: with startups like Amperesand and Heron Power, which are creating solid-state transformers that can accommodate renewables more nimbly and react faster to grid instability. Early deployments are perhaps a year or two away, at which point it will still take time to scale manufacturing.

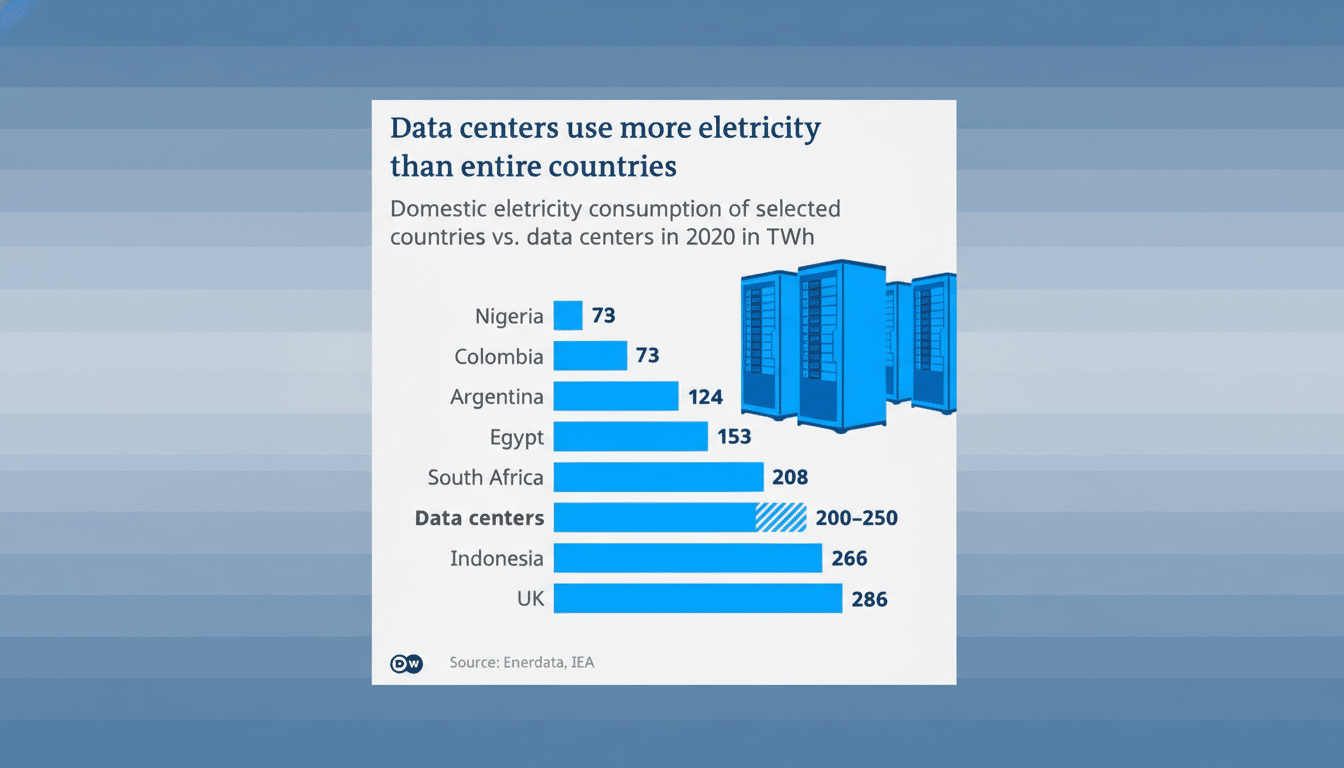

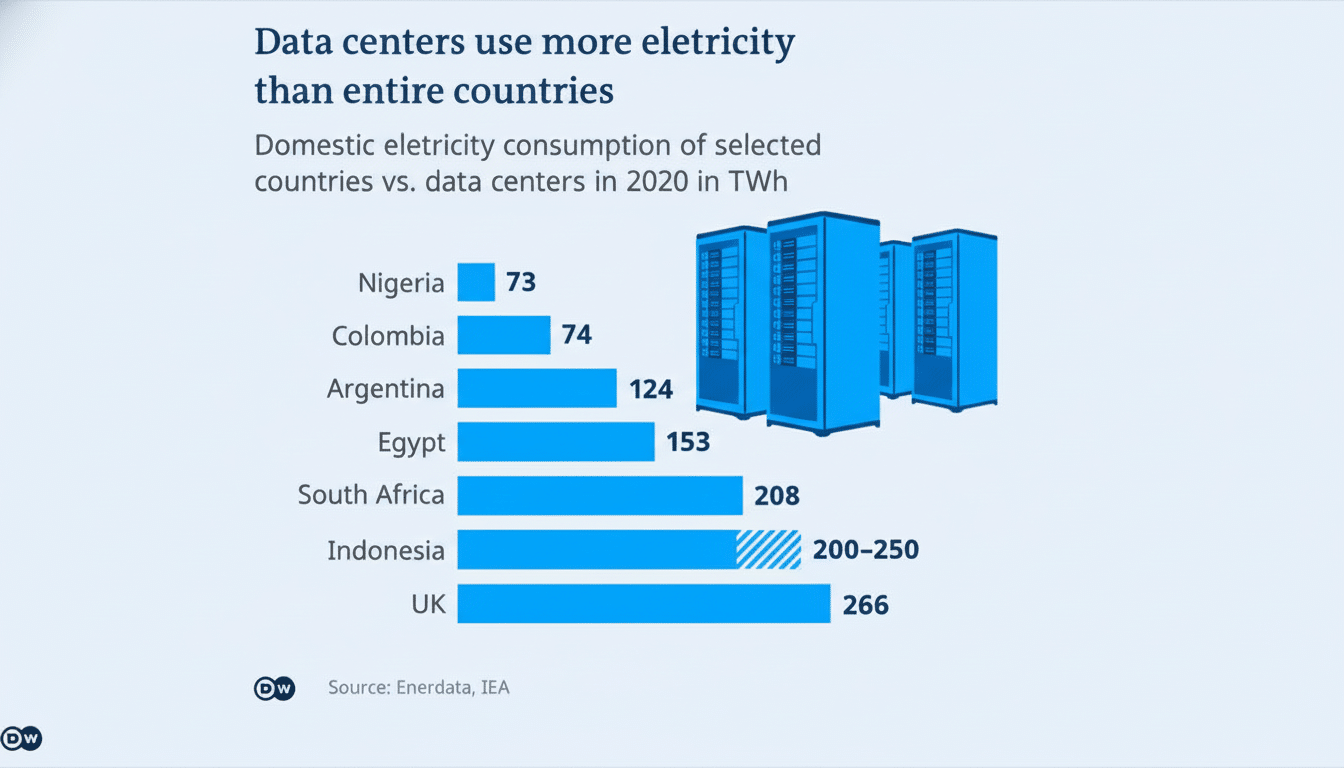

The energy mix driving the data center buildout boom

The IEA forecasts that renewables will provide the majority of new data center power by 2035 under existing policies, with solar the most in favor due to its sharp cost decreases. In the next decade, according to the agency, around 400 terawatt-hours of data center demand will be satisfied by renewables and about 220 terawatt-hours by natural gas. If small modular reactors meet commercialization targets, they could provide some 190 terawatt-hours — an option data center operators are looking at closely for baseload resilience.

AI-specific workloads also alter how operators source energy. 24-hour training jobs favor firm power and long-duration storage; inference may be more compatible with variable generation and demand response. That mix is behind a growing surge in power purchase agreements, behind-the-meter generation and grid services partnerships.

Why the oil investment comparison matters right now

It’s not just symbolic, but a reflection of diverging risk profiles: executives face rising danger they will be fired for growing production, despite recent concerns Wall Street has been too focused on that type of growth. Exploration is contending with price volatility, regulatory pressure and decarbonization mandates, while data centers monetize secular growth in AI, e-commerce and enterprise cloud. The expected growth curve and contract structure in compute outweigh the near-term energy and supply chain headaches for many investors.

None of this takes place in a vacuum. While the above costs can be mitigated by meeting renewable energy needs, we must acknowledge that if the process by which technology such as photovoltaic solar is interconnected to the grid is not made more rapid, if transmission is not expanded and equipment manufacturing capacity remains constrained, then projects will face delays and cost overruns. Policymakers and grid operators are beginning to respond with queue reforms and incentives for grid-enhancing technologies, but how well they will execute, and whether capital continues to outpace hydrocarbons at this scale, remains the open question.

What to watch next as compute outspends oil globally

Three signs will tell whether that investment lead is expanding or narrowing:

- How quickly AI workloads continue to expand

- Interconnection approvals in important hubs

- The supply of transformers and high-voltage hardware

If those trend in the right direction, the IEA’s comparison could signal the start of a long-lasting restructuring of global infrastructure spending — one in which compute, not crude, sets the pace for capital flows.